Disability Income Insurance

What is Disability Insurance?

Disability Insurance Pays Your Bills When Injury or Illness Prevents You From Working

We all work in part to fund our family budget; the mortgage, monthly bills and extras like all the things we buy for our family. If an injury or long-term illness prevented you from working, how would you fund your family budget? Disability insurance replaces your income with a monthly benefit. Your family budget stays funded!

Disability Insurance is an Insurance Policy

Disability insurance is an insurance contract (like life or health insurance) where the insurance company makes a promise to you that if you are unable to work because of an accident or illness, verified by your doctor, the insurance company will pay you a monthly cash benefit equal to 55-75% of your gross income, essentially replacing your take home pay.

In return, you pay a monthly premium cost to the company (based on your income amount, age, and occupation, among other factors).

The Policies are Highly Customizable

Unlike many types of insurance, you can customize disability insurance to fit your needs, and budget:

-The length of benefits if disabled: 5, 10 or 15 years, or until your retirement age; 65, 67 or 70.

-The definition of disability. Paying benefits if you cannot work in a job you are suited for. Or for people with highly specialized occupations you may choose the stronger “own occupation” definition of disability.

-And more options.

If Disabled, Benefits Are Paid Quickly

If you are disabled and cannot work, you will complete a short claim form, and your attending physician will too, providing details for the insurer.

After the waiting period is met the insurer will start paying your benefit each month. You can receive a check in the mail, or most people receive direct deposit into their checking account, just like your paycheck.

And the benefits continue monthly until your doctor clears you for a return to work.

Why You Need Disability Insurance

The best way to understand your need for disability insurance is to visualize what the benefit will do if you are disabled….it will fund your family budget!

Here’s a real life example, a recent client who worked with Chip to purchase her own disability insurance policy. Anna is a Physician’s Assistant in Chapel Hill. Her spouse is currently a stay at home parent with their child, a toddler. Her income is very important to her family’s finances.

Anna’s Physician Assistant Income:

Anna earns $111,500 annually working in the local health system. That $9,285 monthly gross income she earns moves down to $6,500 in monthly take home pay after Federal and State income taxes.

The Family Uses That to Fund Their Family Budget:

Anna and her spouse use that $6,500 for bills, monthly spending, and saving. Here’s a quick, oversimplified look:

-Mortgage: $2,000 -Grocery/Restaurant: $600

-Car Payment: $500 -Family Purchases: $700

-Utilities: $400 -401k Contribution: $400

-Gas: $100 -Student Loan: $300

If Anna Were Disabled, the Disability Insurance Benefit Funds Her Family’s Family Budget!:

When we designed her disability insurance policy we chose a monthly benefit equal to 70% of her current gross income, which translates to $6,500 monthly. And since Anna pays her disability insurance premium costs, if she were disabled and received benefits, those monthly benefits would be received tax free.

Anna and her family can rest easy knowing the disability insurance policy allows for full funding of their family budget, even if she could not work as a Physician’s Assistant because of an injury she sustained or an illness that prevents her from working and earning an income.

We Partner With Many Disability Income Insurance Companies, Including:

Disability Insurance companies excel in different factors of coverage; certain occupations, age groups, benefit options, etc. As an insurance broker (instead of an agent whom represents just one company) we can explore and find the best policy for your specific needs (the best coverage at the most competitive cost).

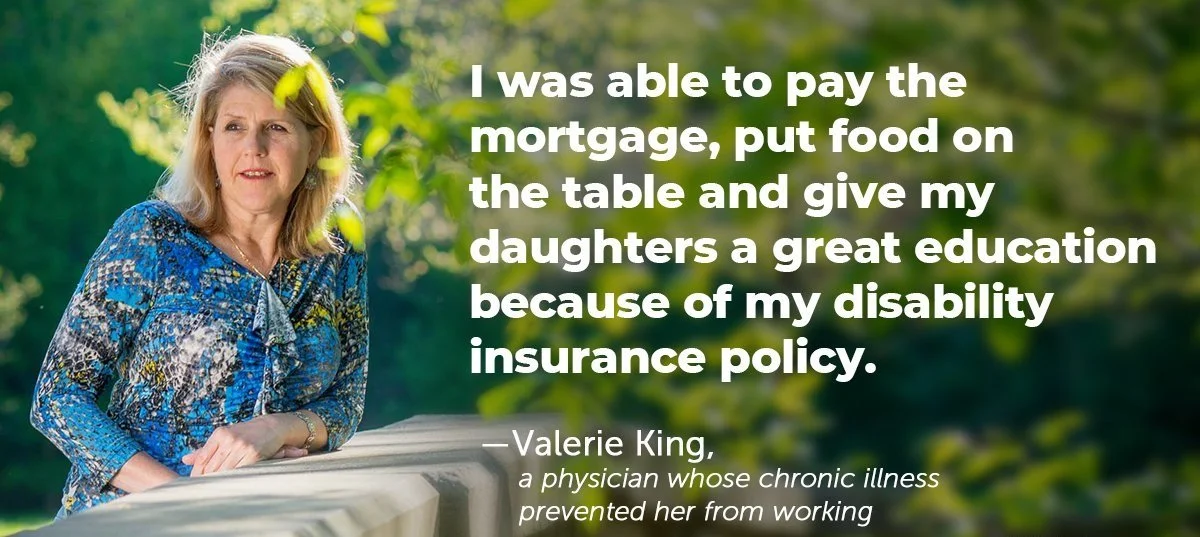

Valerie King’s Disability Insurance Story

“Everything else goes away if you don’t have disability insurance coverage and you can’t work.”

Valerie King was not a believer. When she transitioned from her medical residency to practicing as an emergency room physician, she didn’t think she needed disability insurance. “I could never envision a life without working,” she says. Her insurance professional convinced the young doctor otherwise.

It was wise advice. Although Valerie never thought she would need it, a condition called ulcerative colitis made the decision for her. The disease and a series of surgeries made it impossible for her to carry out her duties, and she found herself unable to practice the profession she loved. It was her disability insurance coverage that allowed her to survive financially and care for her three young daughters who she was raising as a single mother.

“Most people think, ‘It will never happen to me,’” says Valerie. “But the truth is it can—and does. Everything else goes away if you don’t have disability insurance coverage and you can’t work.”

Free Disability Insurance Quote

Complete the below form (designed to take you 2-3 minutes) and submit below. We'll send you a free quote of disability insurance tailored to your coverage needs! You are also welcome to call us for a quote, or with your questions, (919) 357-6637.

Note: Privacy is something we take seriously. The minimum of information is shared with an insurance company to put together a detailed free quote and illustration for you.